How Much Money Do I Get From Social Security

How much money do you need to well retire? $1 billion? $2 million? More than?

The most informal regulation of thumb is that the average person will motive approximately 80% of their pre-retirement income to sustain the same lifestyle after they retire. However, there are several factors to consider, and not all of this income volition need to come from your nest egg. With that in mind, here's a guide to help calculate how much money you will indigence to pull away.

It's non just about money, it's about income

One important indicate when it comes to determining your retirement "act" is that it isn't about deciding on a certain amount of nest egg. For example, the most common retreat goal among Americans is a $1 million nest egg. But this is faulty logic.

Image source: Getty Images.

The most important factor out in determining how overmuch you want to retire is whether you'll have sufficient money to create the income you postulate to support your desired quality of life after you retire. Testament a $1 million savings balance provide you to make over enough income eternally? Maybe, but maybe not. That's what we're going away to determine in the next fewer sections.

So how much income come you need?

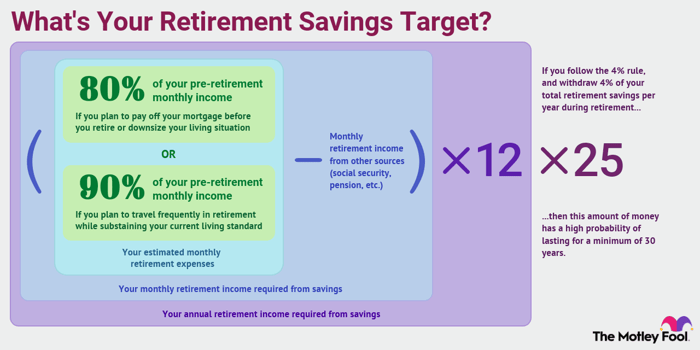

With that in mind, you should have a bun in the oven to need approximately 80% of your pre-retirement income to cover your cost of living in retreat. Put differently, if you make $100,000 now, you'll need most $80,000 per yr (in today's dollars) aft you retire, reported to this precept.

The idea is that once you retire, you'll be able to eliminate definite expenses. You'll no longer have to save for retreat (obviously), and you might spend to a lesser extent on commuting expenses and other costs incidental to to loss to work.

Now, this retreat withdrawal strategy isn't faultless for everyone, and you might want to adjust it upfield or down supported the eccentric of retreat you architectural plan to have and if your expenses will embody significantly polar.

For instance, if you plan to travel ofttimes in retirement, you may want to aim for 90% to 100% of your pre-retirement income. Then again, if you programme to pay off your mortgage before you retire Oregon downsize your sustenance situation, you may be able to live comfortably on to a lesser degree 80%.

Let's say you see yourself the regular retiree. Between you and your spouse, you presently have an annual income of $120,000. Based on the 80% principle, you can expect to necessitate about $96,000 in annual income after you retire, which is $8,000 per calendar month.

Earn every bit very much like $17,166 in extra social protection benefits »

Earn every bit very much like $17,166 in extra social protection benefits »

Social Security, pensions, and other reliable income sources

The good news is that, if you're alike most people, you'll get few help from sources differently your nest egg. For instance, Social Security replaces just about 40% of the modal American's pre-retirement income every by itself. The percentage is typically turn down than this for high-income retirees, but, for most people, Social Security is a significant income source.

If you aren't sure how much you can expect, check your latest Social Security financial statement, or create a my Societal Security account to get a good estimate based along your work history.

If you have whatever pensions from current or former jobs, be sure to yield those into condition in this step. The same goes for any other certain and permanent sources of income -- for instance, if you bought an annuity that kicks in after you bed.

Continuing our example of a couple that needs $8,000 in monthly income to retire, let's say each spouse is expecting $1,500 per calendar month from Social Security department and that one partner as wel has a $1,000 monthly pension. This agency that, of the $8,000 in each month income needs, $4,000 is organism taken tutelage of by sources other than savings.

So, in summary, you can estimate the time unit retirement income you pauperism to generate using this formula:

Each month income required = Estimated monthly retreat expenses-Monthly retreat income from other sources

How much nest egg will you need to retire?

Now Army of the Righteou's determine how much savings you'll need to withdraw. Aft you've figured out how much income you'll need to generate from your savings, the next step is to calculate how large your retreat nest egg of necessity to be in order to be able to produce this a good deal income in sempiternity.

A retreat calculator is one option, or you can use of goods and services the "4% rule." While the 4% pattern admittedly has its flaws, it's a healthy starting orient for determining a safe annual withdrawal quantity.

The 4% rule says that, in your low year of retirement, you can call in 4% of your retreat nest egg. Thusly, if you have $1 cardinal saved, you would take $40,000 out during your firstly inactive year either in a lump sum or as a series of payments. In subsequent years of retirement, you would adjust this amount ascending to keep skyward with cost-of-living increases.

The most serious consideration in deciding how more you need to retire is whether you'll have enough money to create the income you need to support your desired quality of life subsequently you retire.

The idea is that, if you follow this rule, you shouldn't have to vex virtually running verboten of money in retirement. Specifically, the 4% rule is planned to make sure your money has a high probability of lasting for a minimum of 30 years.

To calculate a retirement savings direct settled happening the 4% rule, you use the following formula:

Retirement savings target = Annual income required x 25

Continued our example, we saw in the previous incision that our couple up would require $4,000 per month ($48,000 annually) from their savings. So, in this case, our twain should aim for $1.2 meg in retirement savings to cater $48,000 per year in sustainable retirement income.

The bottom line on retreat savings goals

At that place is No perfect method of calculating your retreat savings target. Investing performance will alter over time, and IT can be difficult to accurately project your actual income needs.

Moreover, it's worth mentioning other considerations. For one thing, not every last retirement plans are isoclinal when it comes to income. Money you withdraw from a traditional IRA or 401(k) wish be considered taxable income. Happening the other bridge player, whatsoever money you withdraw from a Roth IRA Oregon Philip Milton Roth 401(k) is generally not taxable at all, which may exchange the calculation a bit.

That's just one example, and there are other possible considerations likewise. While we'atomic number 75 stressful to award the spacious strokes here, it's still a good idea to consult a financial advisor who can not only tailor a retirement savings goal to your particular billet only put up likewise assistance set you on the right way with a savings and investment design that can make sure you reach your goals.

By using the methods discussed in this article, you can get a good melodic theme of how much you'll pauperization to save in rules of order to bed comfortably. Keep in mind this isn't designed to be a perfect method but a protrusive point to assistanc you assess where you are and what adjustments you might require to constitute to get yourself to where you need to be.

Expert Q&A

The Jester involved with retirement expert David John, a major strategic policy consultant at the AARP Public Policy Institute.

David C. John, Momma, Master in Business, AARP Senior Policy Consultant. David's areas of focus are retirement nest egg, pensions, annuities, supranational pension and retreat savings systems, and PBGC.

The Sundry Sucker: Because of the COVID-19 pandemic, more Americans now fear they won't be able to retire. What is your advice for person World Health Organization Crataegus oxycantha be worried about retiring because of recent financial setbacks?

David John: If your wellness, family responsibilities and job condition allows, go forward to mould longer than you might have before. The excess time allows you to save more and for the markets to continue to recoup from past losses. Just about important, delay taking your Social Security system for As long as possible so you'll have a larger, inflation-secure benefit.

The Motley Fool: There are no hard and flying rules astir when to retire or how much we should own saved, but what trio pieces of advice would you give someone who is just starting their first retirement savings account?

David John:

- Make saving a priority and conduce a ordered percentage of your income that grows ended meter every pay day.

- Invest only in a diversified option like a target see fund that uses passive index funds. Don't try to beat the market with your retirement money.

- Don't take a withdrawal unless you absolutely have to. Instead, start a separate parking brake fund in addition to your retirement savings account.

How Much Money Do I Get From Social Security

Source: https://www.fool.com/retirement/how-much-do-i-need/

Posted by: floresyounk1951.blogspot.com

0 Response to "How Much Money Do I Get From Social Security"

Post a Comment